The global warehouse automation market has contracted, but three segments of the market are seeing significant growth.

Warehousing insights

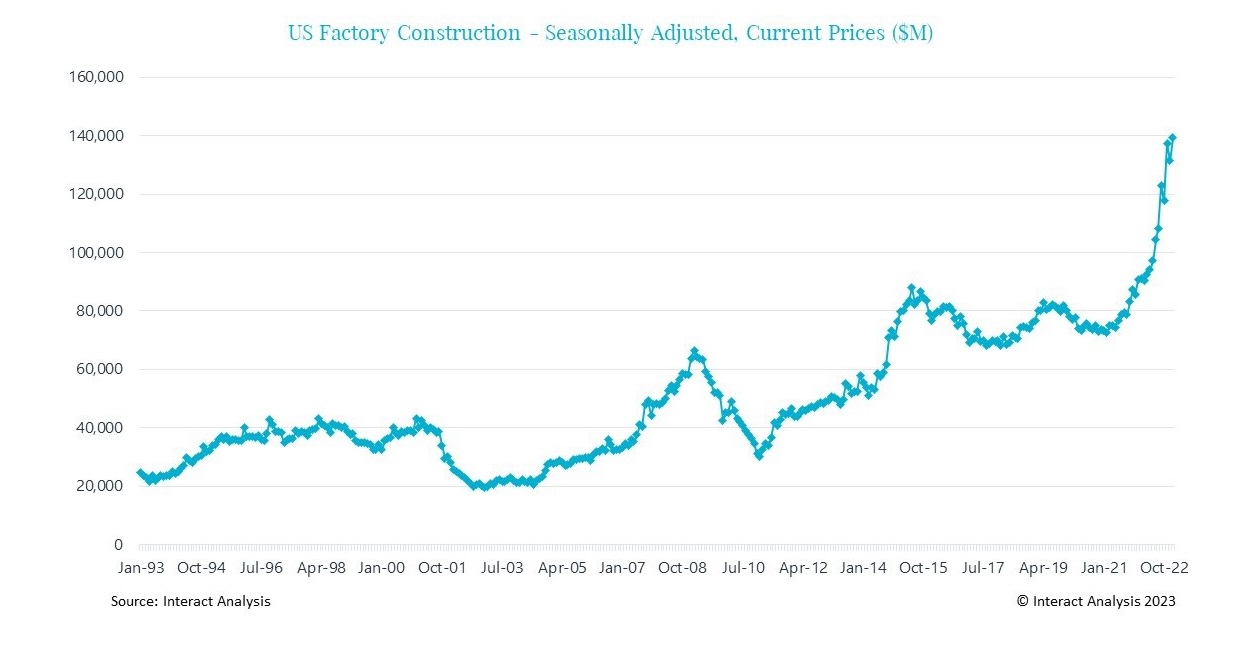

- COVID-19-driven near-shoring of production to the US has led to a surge in factory construction and increased demand for warehouse automation.

- The pet care industry has seen sustained growth due to a surge in pet ownership during the pandemic, driving increased automation investments.

During the pandemic, we saw record levels of warehouse automation investments, driven by higher e-commerce sales and a boom in speculative warehouse construction. However, fast forward to today and the warehouse automation market is struggling with declining order intake and prolonged sales cycles, which led to a contraction in 2022 and another declining year in 2023. Given the inflationary environment and the resulting high interest rates (which aren’t due to come down any time soon), we expect a relatively sluggish 2024 with limited order intake growth.

In light of a troubling macro-economic environment, it’s more important than ever to find market segments that are poised for growth. Indeed, within the wider declining market, there are particular sub-segments experiencing phenomenal growth. We’ve spent the last eight months surveying and interviewing automation vendors and end-customers to identify and quantify these outliers.

This insight will explore three growth markets that are bucking the wider trend and expected to experience significant growth over the coming years. We’ve chosen these growth segments at random from a much wider selection that will be included in the full report.

Manufacturing in the United States

Given the supply chain disruptions caused by COVID-19, several large international companies are in the process of near-shoring and re-shoring their production. The data below shows the amount spent on factory construction in the US, which clearly demonstrates a huge increase in investment in US production capacity. Our initial hypothesis, formed back in 2020, was that this near-shoring would result in higher levels of investments in warehouse automation from manufacturers. In 2022, our assumption was validated as we saw nearly all companies reporting significantly higher revenues generated from the durable manufacturing vertical in the US. We saw a similar trend in Europe, but to a lesser extent than the US.

In addition to the near-shoring trends, the US also announced its Inflation Reduction Act, leading to a large increase in electric vehicle (EV) production in the US. Factories building electric vehicles or related products, such as batteries, tend to be highly automated and often have associated automated logistics systems. Indeed, many of the automation vendors we spoke to as part of our research indicated that they’re receiving a lot more demand from EV manufacturers.

Pet care industry

During the pandemic, the number of furry friends went through the roof. In the United Kingdom alone, the share of households owning pets went up from 40% in 2019, to 59% in 2021, and to 62% in 2022. The more pets there are, the more pet care products are required. For example, Chewy, a US-based pet care e-commerce company, has opened a large number of automated facilities in recent years and says that it will continue to do so. Pan Pacific Pets will be using Attabotic’s storage system, while Pet Supplies Plus invested $53 million in a new distribution center in 2022. Although the pet shop boom isn’t expected to last in the long term, it appears likely to outperform the wider market in the short term.

Healthcare industry

In recent years, the US has introduced a new set of regulations encompassed by the Drug Supply Chain Security Act, which requires manufacturers and distributors to electronically trace drugs all the way from manufacturing to consumption. All trading partners have until November 2023 to incorporate the requisite serial numbers into their processes. While most wholesalers and distributors have invested in the technologies required to comply with the new regulations, our research indicates several companies haven’t invested enough to bring their systems up to speed and will be throwing labor at the problem initially.

In fact, pharmaceutical distributors are calling for the FDA to extend the introduction of the DSCSA by two years, claiming that “industry still does not have the necessary tracing systems in place to comply with the law”.

We’ve spoken to many stakeholders in the drug wholesale and distribution sector, and it’s clear there’s going to be a lot of investment in automation in the coming years as distributors and wholesalers look to become compliant.