The road ahead for manufacturing is bumpy due to disrupted supply chains, labor shortages, and high shipping and energy costs.

COVID-19 saw different regions and industrial sectors suffer at varying rates. At a country level, much depended on the local strategies adopted to deal with the virus. Some were effective and some weren’t.

Despite strong growth, the way out of this crisis is proving to be just as bumpy, as the hangover from the pandemic persists in the shape of disrupted supply chains, labor shortages, and high shipping and energy costs.

Russia (one of the largest natural gas and petroleum producers in the world) is invading Ukraine (one of the largest agricultural producers in the world). So the general air of disruption isn’t going away. Sanctions will cause price rises, hitting both manufacturers and consumers. After COVID-19, this new crisis is something manufacturers could do without.

2021: Reciprocal pressure puts India up top

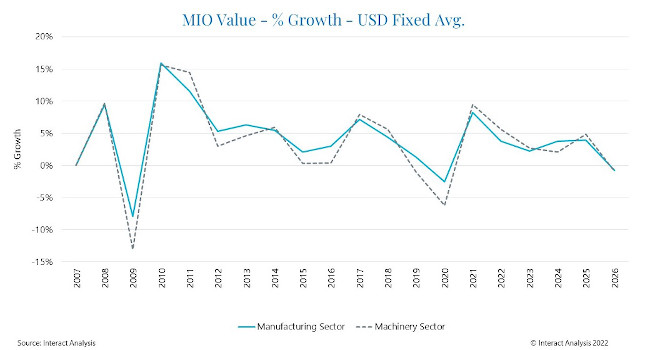

The global manufacturing economy will grow 8.3% in 2021. This does not reflect a manufacturing boom: it’s a recovery from the depths of the pandemic. I call it reciprocal pressure. And it’s a far smaller rebound than we saw in 2010 after the financial crash, when manufacturing growth hit 16%. Why is this? It’s because the COVID-induced manufacturing collapse simply was not half as bad as many (including myself) feared it would be. In 2009 the global depression shrank manufacturing by over 8%. The COVID-induced decline was less than half of this at 3.2% in 2020.

That 8.3% 2021 growth figure, however, masks some incredibly uneven performances by economies during the pandemic. India, for example, saw manufacturing take a hammering in 2020, with swathes of it shutting down. The country lost 16% of its production value compared with 2019. Having fallen so far the recovery was swift, and India was the global leader for manufacturing growth in 2021. Year-on-year growth was 13.4% meaning that India’s manufacturing output was just over $1 trillion.

European recovery hampered by country-specific factors; U.S. remains strong

Europe also struggled badly with the virus; manufacturing slumped by 7.9% and the machinery sector crashed by a whopping 12%. 2021 saw a rapid recovery as a result. But perhaps not as rapid as I might have expected because the European recovery was hampered by a range of country-specific factors, such as Germany’s overdependence on exports. Overall manufacturing output growth for the region was 10% in 2021.

Meanwhile, across the water in the US, where we saw far fewer lockdowns than in Europe, and a huge stimulus package, the 2020 slump in manufacturing was around –3.4%. We have calculated MIO growth to be 10.7% for 2021, taking US 2021 manufacturing output value to $5.27 trillion.

Comparing like with like (or not)

It’s important to understand that we aren’t comparing like with like when we look at the regional picture. The reasons for growth vary wildly depending on local responses to and impacts of Covid in 2020. Europe saw extensive lockdowns in 2020, and still struggled with the virus. In the US there were few lockdowns; factories kept going even while the virus was rampant, at considerable human cost.

In Asia, COVID-19 was dealt with much more effectively. China, for example, which accounts for 69% of production in the region, was the only country featuring in our MIO to see positive growth in 2020, owing to its stringent suppression of the virus. But this means that reciprocal pressure has been less and subsequently MIO growth for 2021 is lower – of the order of 5.8%. In South Korea, on the other hand, growth is being boosted by the post-pandemic semiconductor boom.

2022: Optimism is muted

Going into 2022, we have a number of factors at play. Order books may be full in the machinery sector, for example, but supply chain issues persist and owing to the globalized nature of the manufacturing economy, very few segments are likely to escape unscathed. Reshoring may be a partial long-term answer to some supply problems, in the semiconductor industry, for example, which is currently almost wholly concentrated in Asia, but it isn’t a practicable short-term solution.

The surge in the cost of living is likely to have a negative effect on consumer-orientated manufacturing sectors. And we are expecting to see growth stabilize in 2022 at a much lower level than 2021 – 3.8% for the US, 4.2% for China and 1.5% for India, for example, but it is not necessarily going to take the form of a slowdown. We don’t anticipate that happening until late 2023 or early 2024.

– This originally appeared on Interact Analysis’ website. Interact Analysis is a CFE Media and Technology content partner.